This is the first article in a three-part series on financial-services direct mail in 2025, beginning with market volume and competitive insights.

Direct mail isn’t just holding its ground — it’s accelerating acquisition results in 2025. And when you look at the latest Mintel credit-card direct-mail data, the story becomes clear: the nation’s largest issuers continue to invest heavily in physical mail because, when the pressure is on to win market share, direct mail performs.

In April 2025, more than 285 million credit-card acquisition mail pieces reached consumer mailboxes. That level of volume only happens in channels that demonstrate consistent ROI. And as digital channels become more regulated, more fragmented, and more expensive on a cost-per-acquisition basis, financial marketers continue to rely on the channel that delivers scale, predictability, and measurable lift.

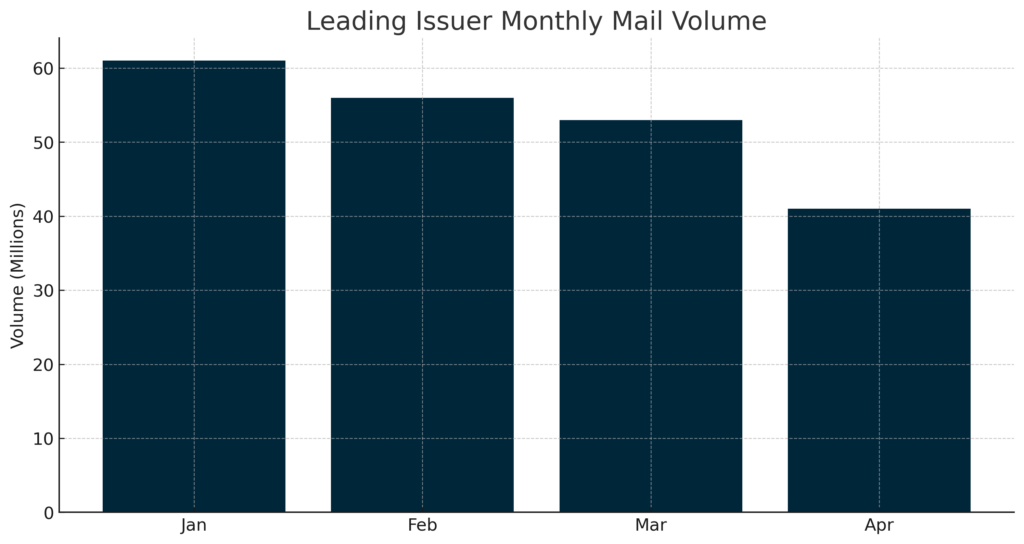

Monthly direct-mail volume for the leading issuer, showing consistent acquisition investment through early 2025.

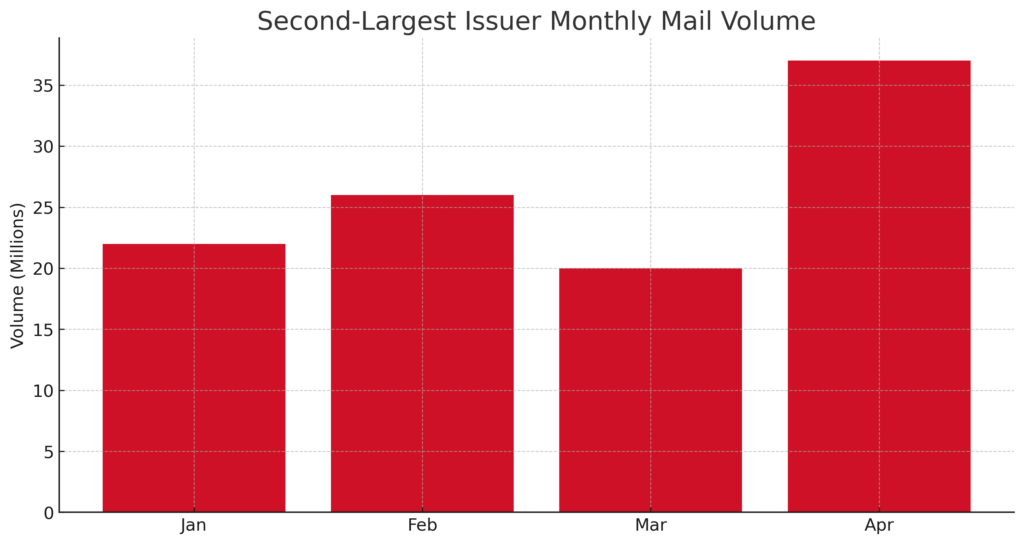

The second-largest issuer demonstrates notable month-over-month acceleration, signaling heightened competition for active credit prospects.

Why Issuers Are Increasing Deployment

One leading issuer maintained the highest overall mail volume through early 2025. Another increased month-over-month deployment by more than 80%. These shifts aren’t noise — they’re signals. When the largest issuers in the country accelerate their direct-mail deployment that quickly, it reflects rising competition for the financially active household.

Meanwhile, other major issuers maintained steady mail volume — a strategy proven to support brand visibility and acquisition throughout fluctuating market conditions.

2025 Industry Momentum Beyond Mintel

While Mintel’s April 2025 dataset provides the most recent issuer-level monthly insight, multiple external industry analyses released later in 2025 indicate that overall direct-mail investment — particularly in financial services — continued climbing throughout the year. These reports point to:

Higher year-over-year direct-mail usage among financial brands

Expanded budgets for acquisition mail

Growth in total U.S. direct-mail volume through mid-to-late 2025

This reinforces what Mintel’s early-2025 snapshot already suggested: direct mail is surging, not slowing.

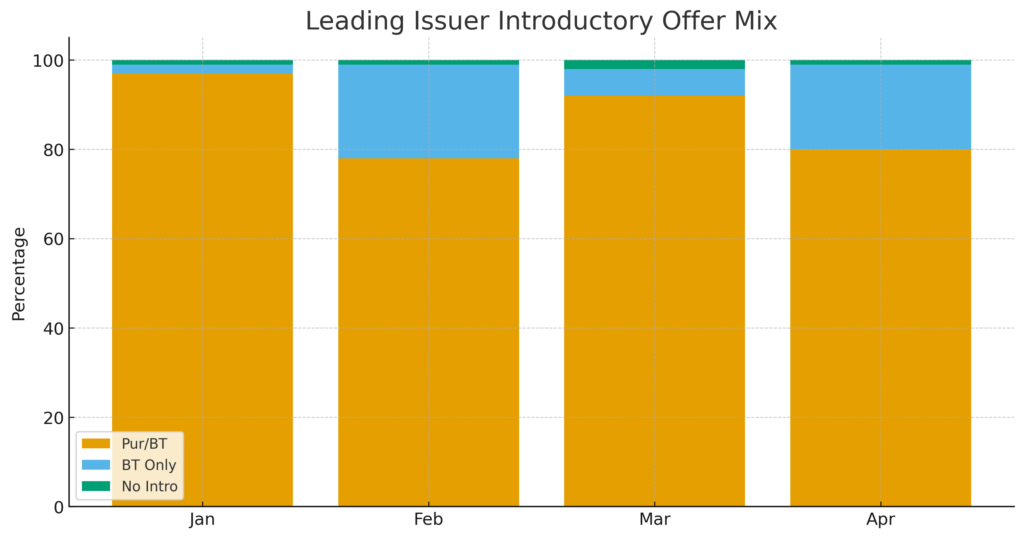

The leading issuer leans heavily on flexible introductory offers, aligning with consumer demand for immediate, high-perceived value.

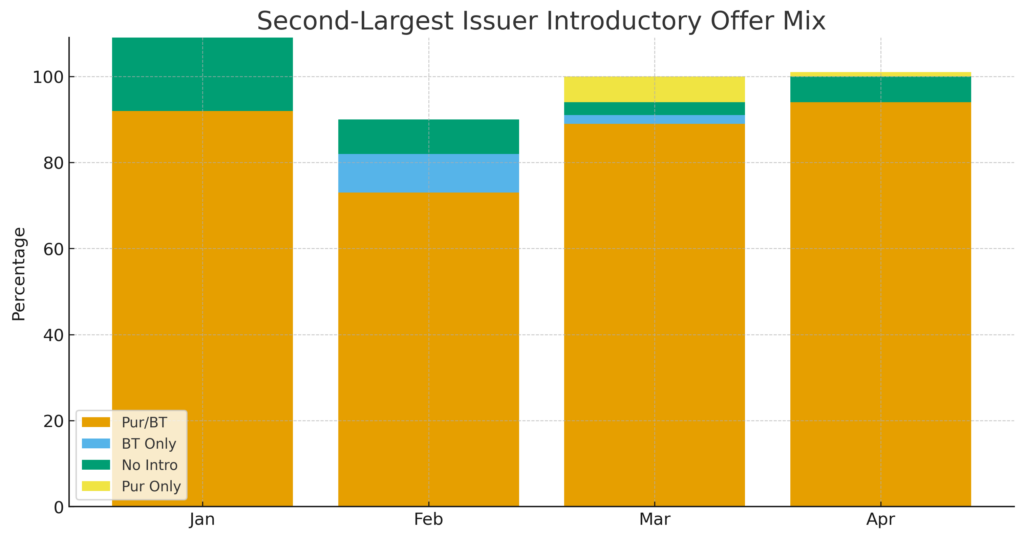

Offer structure variation among top issuers reflects different acquisition strategies and testing approaches within the credit-card market.

Where American Litho Fits In

When issuers scale like this, they depend on production partners who can match their pace. This is where American Litho excels.

Inside our 650,000 sq. ft., fully secure, end-to-end production environment, every step happens under one roof — data, digital presses, envelope converting, finishing, commingling, and postal optimization. That means:

Faster deployment

Greater control

Lower risk

More accurate, repeatable results at enterprise scale

Our HP PageWide fleet — including the T4250, T490, and dual T250 presses — handles massive variable-data versions, rapid A/B tests, and high-velocity acquisition cycles with color accuracy backed by our G7 Master Facility Colorspace certification.

What This Means for Financial Marketers

The mailbox remains one of the few places where:

Competition is visible

Results are trackable

Scale is achievable

Personalization is decisive

Even as the digital landscape shifts, the issuers winning in 2025 are those who pair data-driven offers with high-performance production and postal intelligence.

And that’s the advantage American Litho brings to every campaign.

Executive Takeaways

Mintel’s 2025 data shows strong issuer-level direct-mail deployment and competitive lift.

Outside industry reports indicate that financial-services mail volume continued to rise throughout 2025.

American Litho’s press platform, data environment, and postal intelligence give issuers unmatched speed, precision, and scalability.

Direct mail remains a performance channel — and American Litho provides the firepower behind it.

This is Part 1 of a 3-part series on financial-services direct mail in 2025.

In this first installment, we focus on market volume and competitive trends. Parts 2 and 3 will break down offer strategy and the production technologies shaping performance.